When geopolitical tensions escalate, the media space is often flooded with macro-level theories and abstract economic projections that feel entirely detached from the day-to-day reality of the market. As an active real estate broker dealing daily with high-net-worth individuals and institutional investors in Abu Dhabi, I can tell you that this is not the time for academic posturing. It is a time to look at hard facts, actual numbers, and on-the-ground realities. The market is undergoing a genuine shift: transaction paces are slowing, buyer psychology is altering, and real downside risks are emerging that cannot be ignored.

The Pulse of the Market: Voices from the Ground

Over the past few weeks, the nature of my conversations with clients has fundamentally changed. The pressing question is no longer, “What is my expected ROI in six months?” Instead, it has become, “How do I protect my capital from regional volatility?” We are witnessing a tangible lengthening of decision-making cycles. Investors who were previously ready to close AED 20 million deals on Saadiyat Island or Yas Island are now hitting pause, preferring to hold cash reserves until the geopolitical fog clears.

This shift from an “aggressive speculation” mindset to one of strict “wealth preservation” is not just a sentiment—it is the daily reality in our meeting rooms. The appetite for indiscriminate buying has vanished. Today’s smart investor is meticulously searching for high-quality, tangible assets in strategic locations, showing a strong preference for ready properties or projects backed by highly reputable developers with flawless delivery track records.

The Numbers: Between Historic Highs and Current Slowdowns

To understand our current position, we must look at actual data rather than relying on market mood. Abu Dhabi’s real estate market concluded 2025 with an unprecedented historic performance. The Abu Dhabi Real Estate Centre (ADREC) recorded a record-breaking AED 142 billion in real estate transactions, representing a 44% increase compared to 2024. We saw over 22,400 residential unit transactions, with apartment prices rising by 15.1% and villa prices by 12.2%.

What truly stands out about these figures is the quality of the capital. Cash transactions accounted for 87% of the total residential sales value , reflecting massive market liquidity and low leverage risks. We also kicked off the first quarter of 2026 on strong footing, recording AED 12 billion in sales in the first two months alone.

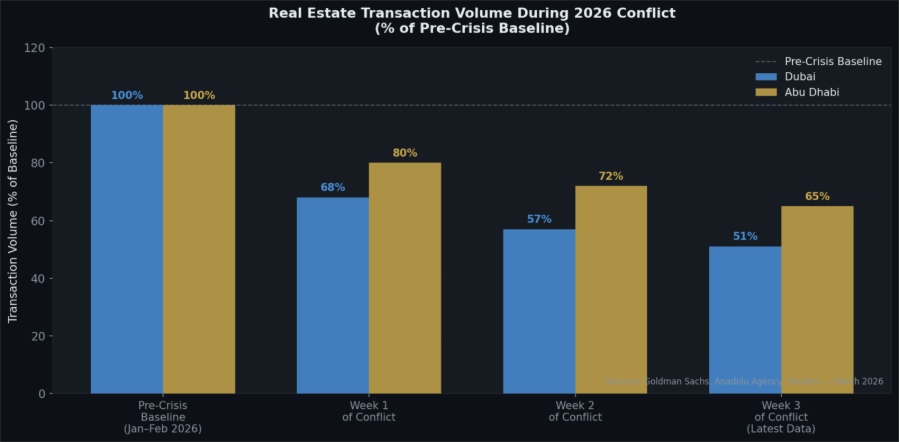

However, the rosy picture of 2025 has collided with a complex geopolitical reality in March 2026. Recent reports, including data from Goldman Sachs, indicate that real estate transaction volumes across the UAE dropped by approximately 37% year-on-year during the first few weeks of the conflict. This on-the-ground decline is real and palpable, proving that even the strongest markets are not immune to temporary shocks in investor confidence.

Downside Risks: What Many Are Not Talking About

Discussing market resilience should not blind us to clear downside risks. Despite its strong economic fundamentals, the Abu Dhabi market faces genuine challenges, particularly in specific segments. First, there is a distinct risk of oversupply in the apartment sector within secondary locations. While ultra-luxury waterfront properties maintain their value due to scarcity, high-density residential projects could face downward pressure on both pricing and rental yields if foreign investment demand wanes.

Second, considering that off-plan sales accounted for 71% of total transactions in 2025, any liquidity tightening or supply chain disruptions caused by regional tensions could impact delivery schedules. This very concern is driving many buyers today toward ready properties, thereby forcing developers of new projects to offer increasingly aggressive incentives to secure capital.

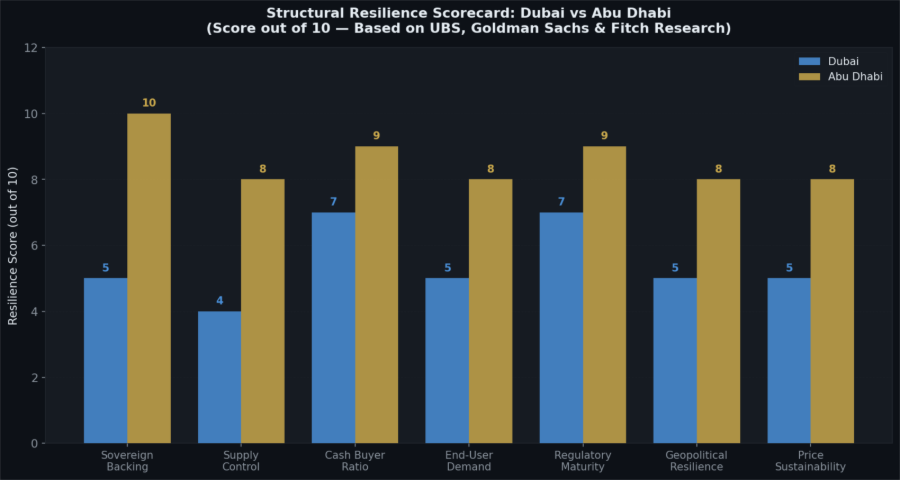

When comparing the regional landscape, a recent report by UBS warned that Dubai might face steeper short-term challenges. An estimated 110,500 residential units are slated for delivery in Dubai in 2026, compared to a historical average of 27,000 units, significantly raising the risk of a supply glut. In contrast, Abu Dhabi has adopted a much more conservative approach, with only 6,500 to 9,000 units expected to be delivered in 2026. While this limits the risk of severe oversupply, it does not eliminate the possibility of a slowdown in the absorption rate of these new units.

A Balanced Perspective: No Magic Shields

It is essential to remain objective; Abu Dhabi is not entirely isolated from its surroundings. While the emirate enjoys massive sovereign backing and a mature regulatory infrastructure, real estate markets are inherently tied to broader sentiment. Even in the most resilient environments, geopolitical friction leads to liquidity contraction and investment hesitation.

We may witness price corrections in Abu Dhabi over the coming months, particularly for properties that saw inflated pricing during the 2025 boom. Premium assets will remain safe havens, but mid-market investment properties and projects in lower-demand areas will undergo a true test of their viability. Acknowledging this reality is what separates a professional investor from a transient speculator.

Looking Ahead: Conservative and Realistic Scenarios

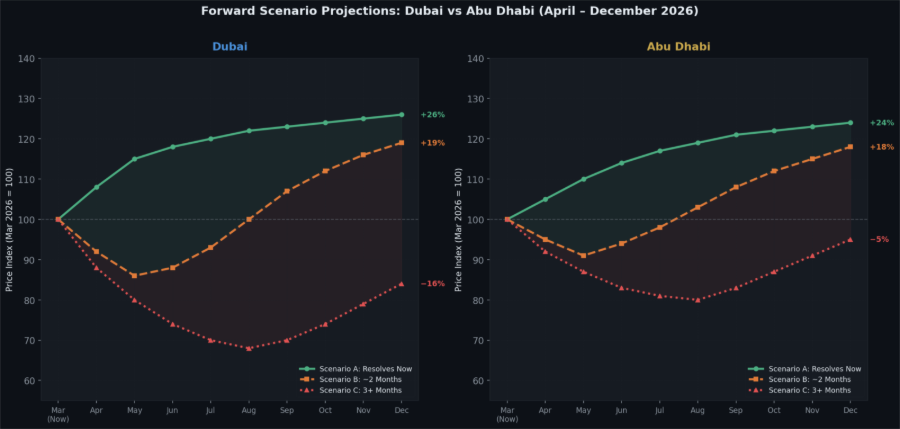

Based on ground-level dynamics and current data, we must recalibrate our forward-looking projections to be more conservative and realistic, stepping away from overly optimistic assumptions.

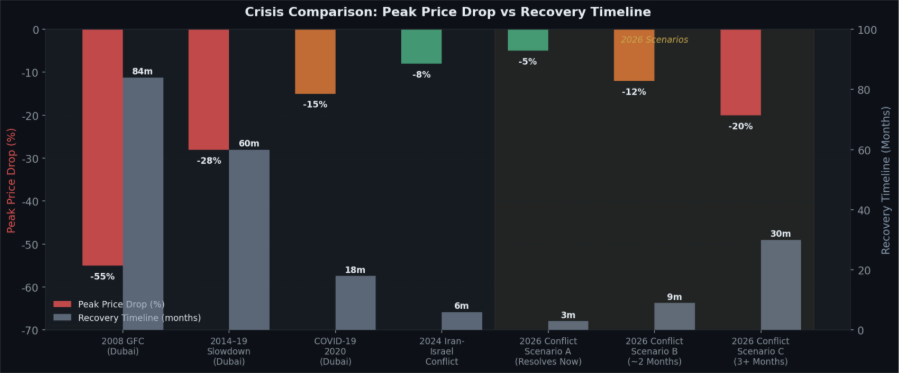

Scenario A: Near-Term Stabilization (Slow Recovery) Even if geopolitical tensions resolve shortly, investor confidence does not return overnight. It will take three to six months for transaction volumes to normalize. Under this scenario, Abu Dhabi prices will stabilize with only marginal growth by year-end, driven primarily by end-users and steady domestic demand.

Scenario B: Prolonged Tensions for Several Months (Transaction Stagnation) If the current climate persists through mid-year, we will see a sustained and noticeable drop in sales volumes. Sellers will hold firm on asking prices due to a lack of mortgage pressure, while buyers will demand steep discounts, leading to a widening bid-ask spread. The result will be transaction stagnation and mild price corrections (around 2% to 5%) in non-prime areas.

Scenario C: Extended Crisis and Broader Regional Impact In the event of a prolonged conflict, the market will face severe stress testing. Foreign direct liquidity will drop sharply, and we may see widespread delays in new project launches. Despite Abu Dhabi’s structural resilience, we could witness an average price decline of 5% to 8%, with the apartment sector taking a significantly harder hit than the luxury villa and master-planned community segments.

Conclusion: Investment Strategy in Times of Uncertainty

As a market, we are going through a natural and healthy filtering process. Smart money does not flee; it repositions intelligently. My direct advice to investors today is this: step away from indiscriminate buying and short-term speculation. Focus strictly on quality. Target ready properties or near-completion projects with stable rental yields, and avoid over-leveraging at all costs.

Abu Dhabi’s real estate market offers a mature investment environment backed by rock-solid fundamentals. However, it requires a mature investor who understands that real estate is a long-term commitment. In times of crisis, true wealth is built by those who possess patience, cash liquidity, and the strategic clarity to acquire premium assets when others hesitate.